Here are the reasons for our viewpoint that Hubbell’s Power segment (known as HPS) will lead the company’s growth over the coming years.

Continue reading Hubbell, Inc. Becoming a Stronger Participant in the Market for Grid Modernization with RFL and Aclara Acquisitions

Category: Mergers & Acquisitions

What to Expect Next: Potential Synergies of the Alstom (Power and Grid) Acquisition by General Electric

As many long-term readers of Newton-Evans’ reports and articles knew from our assessment reported in 2009 there were back then three major contenders for the $7 billion Transmission and Distribution business units of the old Areva T&D Corporation. These were the American firm General Electric, the French corporate combination of Alstom and Schneider Electric, and the Japanese company, Toshiba. In the end the French government simply divided Areva T&D in half, and placed the “T” business into Alstom and the “D” business into Schneider Electric.

On June 21, 2014 GE was informed that Alstom’s board of directors decided to recommend GE’s offer to acquire the Power and Grid business of Alstom Corporation. These units are: Alstom Power (generation assets) and more importantly for this assessment, Alstom Grid, the HV and control systems components of the old Areva T&D business. The “D” business of Areva has now become a core business within the capable Schneider Electric camp of medium voltage equipment offerings.

Newton-Evans Research believes significant benefits to GE’s efforts targeting the global electric power industry will accrue if the company staffs truly work synergistically. Here are six key reasons for this view, in our opinion:

(1) IMPROVED WORLD MARKET ACCESS: GE will gain improved access to European electric power markets and other world regions with long-established relationships nurtured by Alstom and predecessors under the French management and government policies, which may continue under GE ownership, now that the French government is slated to become a significant shareholder investor in Alstom securities. Keep in mind that GE has more than a century of experience and accomplishments in France. I can recall visits to Belfort in eastern France and visiting both GE and Alstom (Areva) factory sites.

(2) ATTAINMENT OF ORGANIC GROWTH: GE Energy Management will again be able to lay claim to some real growth within 24 months of the close of this acquisition. Growth will come from both inorganic sources (via this acquisition – itself worth more than $4 Billion in current year sales of Alstom Grid products, systems and services) and organic growth (through increased interest in, and procurement of all combined GE-Alstom equipment, products and services). Each of the four component businesses of GE Energy Management including: Digital Energy, Industrial Solutions, Power Conversion and Energy Consulting will each benefit significantly if all goes as planned and envisioned in early July 2014. The big issue we see is whether Atlanta and Toronto will report in to Paris, or whether the reverse will be true.

(3) REDUCTION IN OFFERINGS “GAP”: GE will be able to fill several significant product/equipment gaps in its electric power transmission and distribution product line and related automation offerings. This will result in significant mid-term benefits to GE Digital Energy. However, a key issue for GE will be the “branding” of product offerings going forward from midyear 2015.

(4) MARKET-LEADING POSITION IN POWER GENERATION: Alstom’s power business includes assets for power generation such as turbines for coal, gas and nuclear power plants, wind farms while GE is a co-leader in both fossil, nuclear, hydro and renewables businesses.

(5) INCREASED SHARES OF OPERATIONAL CONTROL SYSTEMS: While GE’s EMS offerings have had somewhat limited success beyond North America, it’s DMS, OMS and GIS offerings are well-respected and are high quality offerings. Alstom Grid is a world leader in EMS, with a world-class group of systems for power transmission and distribution. The company’s “e-terra” line of systems is the leading market shareholder among critical T&D operational control systems used in the global electric power industry. The company also has developed a growing customer base among large utilities for advanced distribution network management with its IDMS offering. If the companies’ technical and product marketing teams work together as they have over time on various technical committees (IEEE, IEC, CIGRE et al) and provide smooth cross-systems integration capabilities, the company will be a force to be reckoned with in the world market for control systems. GE has a strong substation modernization/automation business focus across all components (systems, products, intelligent devices, communications equipment) that leads the North American market and is a growing force internationally.

GE Energy Management will likely become a major player in several growing portions of the transmission equipment business, establishing a stronger foothold in the North American and international transmission market segments described below. Together these segments are worth $32-40 billion on a worldwide basis. Newton-Evans’ estimates that Alstom Grid earned about $3.5 billion to $4.1 billion in HV equipment sales in 2013.

Here is our take on the gains to be realized for both electric power infrastructure and electric utility automation and services:

FACTS and Reactive Power Compensation:

ABB is probably the global leader in flexible AC transmission systems and the related reactive power compensation segment of high voltage equipment for transmission networks. Siemens Energy is a strong number two supplier with several others (notably Mitsubishi Electric Power Products, and American Superconductor) also active in North America, and around the world. Alstom Grid and GE are also participants that together could challenge the market leading positions of ABB and Siemens within three years of a merger of product lines.

HVDC Equipment:

Siemens is the market leader in HVDC, with ABB a reasonably close second place share holder and MEPPI the likely third most important player. However, an integrated Alstom Grid-General Electric product grouping would enable the company to attain up to a quarter of the available market shares.

Gas Insulated Substations/Switchgear:

The North American market for High Voltage GIS equipment is in excess of a quarter billion dollars. While Alstom Grid has only a small share (stronger in Canada than in the US), GE Energy could now present itself as a player in this growing market segment of high voltage switchgear. GE would also play a much more important role in international markets where – unlike in North America – GIS equipment is prevalent. Globally, GIS equipment is a 2-3 billion dollar annual market.

High Voltage Bushings:

This relatively small (about $125-150M in annual worldwide sales) market is led by Siemens and ABB. However, the combined Alstom Grid and GE offerings could make GE into a formidable player in this segment.

High Voltage Capacitors:

GE Energy is already the major participant in the North American market for HV capacitors, but globally, ABB is the leader. Alstom Grid, by virtue of its recent acquisition of the Finnish manufacturer, Nokian Capacitors, is also a very strong player in Northern Europe. Together, the product lines could pose a real threat to ABB dominance here (yet another billion dollar global product segment).

High Voltage Circuit Breakers:

Alstom Grid is already a major player globally, and with GE’s “sales boots on the ground” could significantly increase its share in North America and abroad. ABB and Siemens are both very strong manufacturers in this large annual global market of better than $2 billion.

Disconnect Switches:

High voltage disconnect switches are vital components of many transmission systems, and the global market runs to about $500 million annually. GE and Alstom Grid are among the six leading suppliers of disconnect switches in North America, but lag behind Hubbell, S&C and Southern States, some of which offer circuit switchers used for disconnect applications.

Large Power Transformers:

Alstom Grid is number three in the world in terms of large power transformer market share and assets, operating 13 plants with an annual production capacity of more than 130 MVA. GE Prolec is a major North American market force with about a 14% share of the U.S. market. Together, this alliance may become number three in the global market for LPTs behind ABB and Siemens). To do so, the GE-Alstom combine will have to fend off HICO, Hyundai, Toshiba and MEPPI as well as three up-and-coming Chinese manufacturers.

Instrument Transformers:

The market for high voltage instrument transformers had been dominated by specialist “independent” manufacturers until recently. A recent buying spree had Siemens acquiring Trench Electric, Alstom Grid acquiring Ritz and ABB acquiring Kuhlman. Currently, the market for HV IT equipment is shared primarily by these three firms, with GE very active in the MV segment. Together, the combined HV/MV instrument transformer offerings of an integrated GE-Alstom Grid would change the shape of this market, which in North America alone hovers around $100 million, and close to one-half billion dollars worldwide.

Air Core Reactors:

Another component of some transmission network architectures, Siemens-Trench and Alstom Grid-Ritz are key players, with GE also strong and MEPPI further behind, but with a growing share. A number of smaller participants account for a rather large share of this $400 million global business.

Surge Arresters:

Another sizable market in its own right (about $1 billion per year globally) high voltage surge arresters are manufactured by a number of US-based firms such as Hubbell, Thomas & Betts, and Cooper Power, each of which competes quite successfully against the likes of ABB, Siemens and GE.

Automation Systems:

GE’s older XA/21 EMS platform and Alstom Grid’s highly rated E-Terra offerings are both held in high regard around the world, although GE’s systems are mainly installed in the USA. By year-end 2015 and more likely into 2016, General Electric-Alstom Grid will see benefits from world-leading combined market shares in substation automation, protection and control and T&D control systems (energy management, DMS, OMS, GIS and SCADA). Earlier (1990’s era) acquisition efforts have been fraught with initial business unit integration problems (to wit- ABB with its acquisition of the older Ferranti EMS business (Spider v. Ranger offerings) and Siemens-Control Data (Sinault-Spectrum v. Empros).

Substation Modernization:

If protective relays are included in the mix of substation modernization, then the collaborative efforts of GE and Alstom will lead to a global co-leadership market position across the board. Alstom Grid enjoys a strong position with transmission class relays and related MiCOM systems and equipment, and has been fairly strong participant in the global market for substation automation. GE enjoys a strong position in protective relays in North America (number two supplier) and in some Western European and Asian markets, and does make the list of qualified suppliers elsewhere.

Protection and Control:

Internationally, Alstom Grid (with part of the Stafford, UK-based relay business) holds an estimated 16% share of the global protective relay market (outside of the U.S.), estimated by Newton-Evans to be about $2.4-$2.6 billion this year. GE Multilin, based in Toronto, is also a very strong market participant, especially in the Americas, and is the leader in industrial protection and control markets.

T&D Services:

GE is a major participant in T&D equipment repair and services, especially with its transformer repair business, and Alstom Grid outside of North America earns about $550 million per year with its array of high voltage equipment services and global agreements for automation systems maintenance and upgrades.

Let’s not count this as a “done deal” quite yet. I do believe it is now very likely to be seen through by all parties (GE, Alstom, French government, possibly various international courts). The important role of Alstom’s minority shareholders and their reaction to the GE acquisition is somewhat unclear as is the role the French government’s strong minority ownership position will play. GE has made significant concessions regarding job retention among the French workforce, and has promised to add another 1000 jobs in the country. This could have ripple effects on its global workforce, especially if workforce reductions take place.

The following chart (used with permission of General Electric) illustrates the current state of the acquisition and the alliance formation.

Here We Go Again: Potential Synergies of an Alstom (Power and Grid) Acquisition by General Electric:

As many long-term readers of Newton-Evans’ reports and articles knew from our assessment reported in 2009 there were then three major contenders for the $7 billion Transmission and Distribution business units of the old Areva T&D Corporation. These were the American firm General Electric, the French corporate combination of Alstom and Schneider Electric, and the Japanese company, Toshiba. In the end the French government simply divided Areva T&D in half, and placed the “T” business into Alstom and the “D” business into Schneider Electric.

This past week, there have been widely circulated rumors of another attempt by GE to acquire Alstom’s power business, principally Alstom Power (generation assets) and Alstom Grid, the HV component of the old Areva T&D business. The “D” business of Areva is now squarely in the capable Schneider Electric camp of medium voltage equipment offerings.

Newton-Evans Research believes there could be significant benefits to GE’s efforts targeting the global electric power industry if the company’s current purported acquisition attempts bear fruit. There are four key reasons for this view, in our opinion:

(1) As reported by others, GE will gain improved access to European and other world regions with long-established relationships nurtured under the French management and policies, which are likely to continue under GE ownership.

(2) GE Energy Management will again be able to lay claim to some real growth within 24 months. These increases will come from both inorganic growth (via this potential acquisition – itself worth about $4.5 Billion in current year sales of Alstom Grid products, systems and services) and organic growth (through increased interest and procurement of all GE Energy Management equipment, products and services). The four component businesses of GE Energy Management include: Digital Energy, Industrial Solutions, Power Conversion and Energy Consulting. These will each benefit significantly.

(3) GE will be able to fill several significant product/equipment gaps in its electric power transmission and distribution product line and related automation offerings. This will result in significant mid-term benefits to GE Digital Energy.

(4) Alstom’s power business includes assets for power generation such as turbines for coal, gas and nuclear power plants, and wind farms. Alstom Grid offers a world-class group of control systems for power transmission and distribution as well as many leading transmission-class equipment offerings. The company’s “e-terra” line of systems is the leading market shareholder among critical systems used in the global electric power industry.

A successful acquisition by General Electric would provide the firm with world-leading combined market shares in substation automation, protection and control and T&D control systems (energy management and SCADA). GE Energy Management would become a major player in several growing portions of the transmission equipment business, establishing a stronger foothold in the North American and international transmission market segments described below. Together these segments are worth $32-40 billion on a worldwide basis. Newton-Evans’ estimates that Alstom Grid earned about $3.5 billion to $4.1 billion in HV equipment sales in 2013.

FACTS and Reactive Power Compensation: ABB is probably the global leader in flexible AC transmission systems and the related reactive power compensation segment of high voltage equipment for transmission networks. Siemens Energy is a strong number two supplier with several others (notably Mitsubishi Electric Power Products, and American Superconductor) also active in North America, and around the world. Alstom Grid and GE are also participants that together could challenge the market leading positions of ABB and Siemens within three years of a merger of product lines.

HVDC Equipment: Siemens is the market leader in HVDC, with ABB a reasonably close second place share holder and MEPPI the likely third most important player. However, an integrated Alstom Grid-General Electric product grouping would enable the company to attain up to a quarter of the available market shares.

Gas Insulated Substations/Switchgear: The North American market for High Voltage GIS equipment is in excess of a quarter billion dollars. While Alstom Grid has only a small share (stronger in Canada than in the US), GE Energy could now present itself as a player in this growing market segment of high voltage switchgear. GE would also play a much more important role in international markets where – unlike in North America – GIS equipment is prevalent. Globally, GIS equipment is a 2-3 billion dollar annual market.

High Voltage Bushings: This relatively small (about $125-150M in annual worldwide sales) market is led by Siemens and ABB. However, the combined Alstom Grid and GE offerings could make GE into a formidable player in this segment.

High Voltage Capacitors: GE Energy is already the major participant in the North American market for HV capacitors, but globally, ABB is the leader. Alstom Grid, by virtue of its recent acquisition of the Finnish manufacturer, Nokian Capacitors, is also a very strong player in Northern Europe. Together, the product lines could pose a real threat to ABB dominance here (yet another billion dollar global product segment).

High Voltage Circuit Breakers: Alstom Grid is already a major player globally, and with GE’s “sales boots on the ground” could significantly increase its share in North America and abroad. ABB and Siemens are both very strong manufacturers in this large annual global market of better than $2 billion.

Disconnect Switches: High voltage disconnect switches are vital components of many transmission systems, and the global market runs to about $500 million annually. GE and Alstom Grid are among the six leading suppliers of disconnect switches in North America, but lag behind Hubbell, S&C and Southern States, some of which offer circuit switchers used for disconnect applications.

Instrument Transformers: The market for high voltage instrument transformers had been dominated by specialist “independent” manufacturers until recently. A recent buying spree had Siemens acquiring Trench Electric, Alstom Grid acquiring Ritz and ABB acquiring Kuhlman. Currently, the market for HV IT equipment is shared primarily by these three firms, with GE very active in the MV segment. Together, the combined HV/MV instrument transformer offerings of an integrated GE-Alstom Grid would change the shape of this market, which in North America alone hovers around $100 million, and close to one-half billion dollars worldwide.

Air Core Reactors: Another component of some transmission network architectures, Siemens-Trench and Alstom Grid-Ritz are key players, with GE also strong and MEPPI further behind, but with a growing share. A number of smaller participants account for a rather large share of this $400 million global business.

Surge Arresters: Another sizable market in its own right (about $1 billion per year globally) high voltage surge arresters are manufactured by a number of US-based firms such as Hubbell, Thomas & Betts, and Cooper Power, each of which competes quite successfully against the likes of ABB, Siemens and GE.

Automation Systems: GE’s long-established XA/21 EMS platform and Alstom Grid’s highly rated E-Terra offerings are both held in high regard, although GE’s systems are mainly installed in the USA. Earlier (1990’s era) acquisition efforts have been fraught with initial business unit integration problems (to wit- ABB with its acquisition of the older Ferranti EMS business (Spider v. Ranger offerings) and Siemens-Control Data (Sinault-Spectrum v. Empros).

Protection and Control: Internationally, Alstom Grid (with part of the Stafford, UK-based relay business) holds an estimated 16% share of the global protective relay market, estimated by Newton-Evans to be about $2.2-$2.4 billion on an annual basis. GE Multilin, based in Toronto, is also a very strong market participant, especially in the Americas, and is the leader in industrial protection and control markets.

T&D Services: GE is a major participant in T&D equipment repair and services, especially with its transformer repair business, and Alstom Grid outside of North America earns about $550 million per year with its array of high voltage equipment services and automation systems maintenance agreements.

We will soon see learn whether and how the French government will allow Alstom to sell off all but its transportation business to a “foreign” company. GE will likely have to make significant concessions regarding job retention among the French workforce. This could have ripple effects on its global workforce.

Market Trends Digest

A special December 2013 edition of the Newton-Evans Research Company’s Market Trends Digest is now available on our website. This edition looks at some of the studies Newton-Evans has put together in 2013. Also, see some preliminary results from our study of the World Market for Substation Automation & Integration 2014-2016, and read two articles by our CEO Chuck Newton:

A special December 2013 edition of the Newton-Evans Research Company’s Market Trends Digest is now available on our website. This edition looks at some of the studies Newton-Evans has put together in 2013. Also, see some preliminary results from our study of the World Market for Substation Automation & Integration 2014-2016, and read two articles by our CEO Chuck Newton:

1. ASAT and Alstom Grid: One Year Post-Merger

2. Cyber-security: Still Time to Heed the Warning Signals

ABB and Tropos Networks: Adding Another Company to ABB’s Basket of Smart Grid “Goodies” alongside the Thomas & Betts and Ventyx Acquisitions

The brief ABB announcement of June 1, coupled with Tropos Networks CEO’s note to friends of the company on June 4, highlight this new acquisition achievement on the part of ABB’s strategic planning groups based in Switzerland (and Germany, and Sweden, and the U.S.A.).

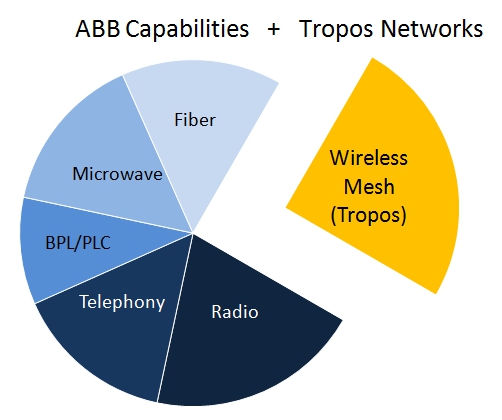

Some readers may not be aware that ABB is a key global player in the utility telecommunications field, winning contracts annually worth hundreds of millions of dollars with its own extensive communications equipment offerings, and supplemented by one of the world’s largest telecommunications network design and development service organizations.

Internationally, many countries outsource the design and development/upgrading of telecommunications networks across the energy spectrum. This is especially true for the developing regions of the world. Key participants in this billion dollar-plus marketplace include the global control systems companies such as Siemens and Alstom Grid, along with ABB. Other key participants in energy telecommunications network development include Alcatel, DIMA, RFL, Selta and Telvent.

Let’s take a closer look at this key ABB acquisition. First, keep in mind that one of the few “gaps” remaining in ABB’s rather pervasive communications offerings is wireless mesh technology. This gap is found in the wireless mesh portion of Tier Two network requirements, and may well extend to “Tier Three” level of utility/energy telecommunications – the field area networks required for distribution automation (not to the NAN or to the meter). ABB has a long and successful history of providing telecommunications systems for Tier One (backbone network infrastructure) and much of Tier Two (backhaul) networks for utilities and energy companies around the world, mainly outside of North America. This opens many doors to ABB clients who have worked with the company in the development of the first two tiers, and who are preparing for additions to Tier Two and work on Tier Three network development. See the chart below.

(c) 2012 by Newton-Evans Research Company

ABB is a highly regarded telecommunications equipment manufacturer (or OEM buyer) in just about every other communications technology area that impacts energy and manufacturing industries, including multiplexing, teleprotection, local area network switches, power line carrier equipment, microwave systems and voice communications. Its wide ranging “Fox-family” product offerings have played a key role in its success in energy telecommunications. ABB engineering skillsets and capabilities can be found in radio, microwave, telephony, fiber (SONET and SDH), BPL and PLC technologies.

Tropos Networks, a 12 year-old privately-held Silicon Valley firm, has grown from start-up status to leader, and an international market participant, in the growing market for wireless mesh technology to support smart grid initiatives, (especially for advanced metering infrastructure, and to some extent for distribution automation) and has a leading position in the provision of municipal/metro area broadband services. The company has shipped some 60,000 routers to more than 850 customers in 50+ countries to date.

However, reading between the lines of this important acquisition, in addition to gaining wireless mesh products, the synergistic benefits accruing to ABB also include the small but strong engineering and support services staff of Tropos Networks, which now will be able to tackle assignments yet to be won by ABB that are further afield from its North American roots. This service capability supplements the company’s highly touted line of wireless mesh equipment. Tropos Networks products and services will also gain a market position in the gas/oil pipeline business and in certain industrial and mining applications where wireless mesh technology can be used as an adjunct with other specialized ABB-developed communications approaches. Freshen up those passports, Tropos staff!

The recent Newton-Evans publication “Global Study of Data Communications Usage Patterns and Plans in the Electric Power Industry: 2011-2015” may be a valuable resource in your company’s plans for the upcoming re-development of grid telecommunications infrastructure. Interested readers can download a brochure and excerpts from this report series on our “reports” tab at www.newton-evans.com .

Eaton Corporation Buying Cooper Industries: Cleveland meets Houston (via Maynooth, Ireland): and, more to the point for the Electric Power Community, Pittsburgh meets Waukesha

Looking Ahead to The Likely Impact on the Electric Power Industry

On May 21, 2012, Eaton Corp. formally concluded an agreement to purchase Cooper Industries PLC in a cash-and-stock deal valued at more than $11 billion. The combined power-related operations will provide a significantly expanded market position in some key growth areas of the worldwide electrical power and distribution industry and positions the combined business entity as a key participant in the evolving “smart grid” marketplace. Together, these firms earned $21.5 billion in 2011 revenue.

The deal, as publicly announced, would create a company (to be known as Eaton Global PLC) that manufactures products and provides a range of power-related services for a wide range of electrical uses, from power grids and lighting to electrical, hydraulic and transmission systems for vehicles, the aerospace industry and the military.

This combined revenue base of $21.5 billion is larger than that of some other major players in the electric power industry (such as Alstom Grid) but is short of global leaders like ABB ($38B), GE ($45 B), Schneider Electric ($29 B) and Siemens ($36B). However, when one takes away the “power generation” revenues of ABB, GE and Siemens, the revenue differences shrink considerably. On the other hand, some units of Eaton Global are themselves only tangentially involved in the electric power industry.

The new company is likely to be called Eaton Global Corp. PLC, planned to be incorporated in Ireland and headed by Eaton Chairman and CEO Alexander Cutler. The deal will first need shareholder approvals at both companies and acceptance by the Irish High Court. The deal is expected to conclude in the fourth quarter (late Autumn) of 2012.

Interesting times indeed! A quick review of Eaton’s Electric Distribution and Control business in North America (and Eaton Electrical internationally) together with a review of the Cooper Power Systems offerings leads us to believe the following:

- Point One: Cooper is a leader in T&D infrastructure and first level smart grid (non-metering), and in several low voltage areas (lighting, small load management) while Eaton is a very strong player in the middle area (commercial and industrial enterprises, some utility-derived revenues and some residential market revenues). In the oil/gas energy field, it would be analogous to stating that Cooper is active in the upstream and downstream aspects of the business, while Eaton is a mainstay in the midstream arena.

- Point Two: The Eaton C-H line of protective relays will benefit with the inclusion of Cooper Power’s Edison line of digital relays.

- Point Three: Together, both companies’ lines of protective relays will move them to a combined revenue position behind SEL, GE and ABB, moving up on Basler, ahead of Beckwith and others.

Here are Newton-Evans’ first impressions of how the competitive landscape will likely be changing with the synergistic effects of this combined corporate entity:

Protective Relays

Effect on Eaton Global: The new company will benefit from combined offerings (complementary)

Effect on the Industry: The combined operations will move the new company into fifth place in North American market shares.

Automation and Control Products

Effect on Eaton Global: Positive effect on new company’s “smart grid” market position and market perception.

Effect on the Industry: Provides solid array of offerings vis-à-vis GE, ABB, Siemens, Schneider.

Circuit Protection

Effect on Eaton Global: The positive and complementary offerings of Eaton Electrical and Cooper Bussman will help the new company grow its position.

Effect on the Industry: Most likely Schneider will see increased competitive thrust around the world.

PQ Monitoring

Effect on Eaton Global: Will be viewed as a true international provider of power quality monitoring, moving up on the global stage in this industry segment.

Effect on the Industry: Likely competitive impact on mid-size firms active in PQ market. (Megger, Dranetz, Power Monitors and several others).

T&D and Power Related Services

Effect on Eaton Global: A truly wide-ranging combined offering from T&D services to industrial, commercial and even residential power-related services.

Effect on the Industry: Will not “steal” shares from others as much as help the total services market (capacity) domestically and internationally. Will still gain competitively vis-a-vis less well rounded offerings of other global services providers.

Cooper Industries

Founded: 1833

Number of Employees: 31,000

Annual Revenue: $5.4 Billion (Cooper Industries), $1.3 Billion (Cooper Power Systems)

o Cooper Power Systems has been meeting electrical distribution needs since 1985, and the companies that make up Cooper have been serving the industry even longer. These companies include: McGraw-Edison, RTE, Kearney, Edison, Combined Technologies, Kyle, Lin Material, McGraw, and Electromanufacturas, SA (Mexico).

o These Cooper Power subsidiary companies helped shape modern electrical distribution systems with advances in overcurrent and overvoltage protection, switchgear, underground distribution, and other product developments.

o Protective Relay Products and Services

Cooper Power Systems manufactures a wide range of medium and high voltage electrical equipment, components and systems for the utility and industrial markets. Used in substations, overhead, underground and in-plant medium voltage distribution systems, the products include:

o Single and three-phase overhead and pad-mounted transformers, substation transformers, power capacitors and controls, voltage regulators and controls, reclosers, pad-mounted switchgear, air-break switches, vacuum switches, sectionalizers, fault interrupters, current-limiting fuses, surge arresters, cable connectors and accessories, transformers components, line construction materials, tools and grounding equipment, faulted circuit indicators, protective relays, SCADA system software, distribution automation equipment, power systems analysis software, and system studies and event measurement services.

In 1998, the company introduced the NOVA solid insulation reclosers and the STAR faulted circuit indicator. In 1999, Cooper introduced the Pathfinder faulted circuit indicator and high firepoint dielectric fluid.

Edison Relays

The Edison line of relays is comprised of 18 compact, draw-out relays which are identical in appearance and operation. Edison relays are designed with ease of use in mind. Offering state of the art performance, all Edison relays feature an easy to use front panel interface that will have you up and running in minutes, rather than hours or days as with most other relays. And since all relays share the same interface, the knowledge you gain from using one relay is transportable to every other relay in the line. All Edison relays feature Modbus communications for easily interfacing to SCADA or automation systems.

DIN Rail Mount Relays

Cooper also offers three very compact, powerful, and economical DIN rail mount relays covering overcurrent and motor applications.

Eaton Corporation Company Overview

Founded: 1911

Sales (2011): $16.1 billion

# of employees: 73,000

Eaton Corporation is a diversified power management company and a global technology leader in electrical components and systems for power quality, distribution and control; hydraulics components, systems and services for industrial and mobile equipment; aerospace fuel, hydraulics and pneumatic systems for commercial and military use; and truck and automotive drivetrain and powertrain systems for performance, fuel economy and safety. Eaton has approximately 75,000 employees and sells products to customers in more than 150 countries. For more information, visit www.eaton.com.

Protective Relay Products and Services

Control and automation equipment include contactors and motor starters, variable speed drives, photoelectric and proximity sensors, PanelMate video control panels, microprocessor-based control and protection devices, as well as pushbuttons and switches, all designed to enhance factory performance.

Power distribution equipment includes a family of circuit breakers, ranging from miniature breakers rated from 120 volts up to world-class vacuum breakers rated up to 38 kilovolts. Other products of this division include integrated facility systems, LV circuit breakers, panel boards, power management, surge protection, switchboards and transfer switches.

The company’s power management protection relays include:

MP3000 Motor Protection Relay – Advanced microprocessor-based motor protection relay that is easy to set up and use. It monitors, controls and protects three-phase induction motors of any size or voltage level against overload, thermal damage to rotor or stator, electrical faults, and excessive starting, and many process equipment failures.

MP4000 Motor Protection Relay- MP-4000 motor protection relay combines all the features required to ensure protection, fault diagnostics, power metering and communication for induction and synchronous motors. The MP-4000 expands upon industry-leading protection, control and diagnostics found in the MP-3000 by adding voltage inputs from Voltage Transformers (VT).

MD3000 Differential Relay- Stand alone self balanced differential protection for critical motors and generators.

DT3000 Feeder Protection Relay – Three phase and ground microprocessor-based overcurrent protection suitable for medium voltage feeder applications, detect and protect against overcurrent faults using ANSI, IEC and thermal curves, with zone interlocking to give you the flexibility to protect your bus without having to add additional CTs.

FP4000 Feeder Protection Relay – Multifunctional microprocessor-based feeder relay with complete current and voltage protection, metering, control and communications in a fixed case package. Multiple setting groups to reduce arc flash energy and zone selective interlocking for bus protection, without having to add additional CTs or relays. Its programming capabilities make it ideal for transfer schemes.

FP5000 Feeder Protection Relay – Multifunctional microprocessor-based feeder relay with complete protection, metering, control and communications in a fixed case or draw-out package. Multiple setting groups to reduce arc flash energy and zone selective interlocking for bus protection, without having to add additional CTs or relays. Its programming capabilities make it ideal for transfer schemes.

Initial Take on the January 30, 2012 ABB Acquisition of Thomas & Betts

ABB now “Walking in Memphis” with Thomas & Betts, after singing “Georgia on My Mind” with its 2010 purchase of Ventyx and the “Song of Arkansas” for its 2011 acquisition of Baldor Electric.

After ABB’s May 2010 acquisition of Ventyx that now appears to have strengthened its hand somewhat in the control center-based systems market for EMS, SCADA and DMS (see www.newton-evans.com/?p=646 ), and the company’s follow-on purchase of Baldor Electric Company (Fort Smith, Arkansas), a leader in electric motor manufacturing, ABB has now announced its intent to acquire Thomas & Betts. T&B is a leading supplier of low voltage gear, and a respectable share participant (via its own recent acquisition of Joslyn Hi Voltage) in the market for medium voltage switchgear. Among its products serving the utility and construction markets are: digital static transfer switches, integrated systems – dual feed & static switch PDUs, power distribution systems, circuit management, industrial UPS, surge protection devices and power quality services are among its MV/LV products.

Joslyn Hi-Voltage manufactures power transmission and distribution equipment for electric utilities. The company’s offerings include reclosers, sectionalizers, capacitor switches and controls, transfer switches, distribution automation equipment, disconnect switches, load break switches, underground switches, and VacStat vacuum interrupter monitors. Fisher Pierce distribution products manufactured by Joslyn Hi-Voltage include Powerflex and AutoCap capacitor controls and Smartset software, faulted circuit indicators (FCIs), line post current sensors, and Smartlink communications.

So, what’s behind the spate of U.S. acquisitions made by ABB over the past 24 months? Here are four solid reasons that we think support ABB’s strategic and decisive actions:

First, the strategic planners within ABB are certainly looking to strengthen the company’s position in the three related utility-centric markets of power generation, transmission and distribution. Ventyx has helped with the company’s total array of “smart grid” related offerings with its IT and OT capabilities. Baldor had provided ABB with additional inroads to the motor market, and now T&B will provide the company with access and distribution channels for low voltage products, and help fill in product line gaps with its Joslyn HV/MV product offerings.

Secondly, look at the gain in ABB’s access to the construction and industrial segments, both of which may see some upswing by mid-2012. T&B plays an important role as well in serving the needs of mid-size utilities across the country and to some extent, internationally. This provides ABB with additional openings into the public power utilities and cooperative utility communities.

Thirdly, I think ABB has correctly identified the “new elephant” in the global electric power marketplace as Schneider Electric. This acquisition marks the first significant industry reaction to Schneider’s key role around the world in low voltage equipment (as well as some MV offerings by virtue of the division of assets of the former Areva T&D) and Schneider’s extremely well-developed marketing channel strategy.

Fourthly, is ABB’s response to the near-term global economic outlook. By virtue of its continuing focus on North American acquisitions, ABB is avoiding the as-yet unresolved Euro-crisis in terms of purchase prices and values, and near-term European market outlook. Coupled with the fact that North American construction and industrial activity will likely pick up the pace this year (given what we have seen thus far into 2012), the acquisition certainly makes sense to me.

As far as downsides to the string of acquisitions, the biggest complaint I have seen among financial analysts commenting in the press for all three acquisitions, is the premium paid for these companies, relative to earnings, market value or recent year revenues. On the other hand, ABB has the financial resources and the access to capital markets that together enable the company to take these decisive strategic actions to improve its overall market position in North America, and around the world.

– Chuck Newton

Schneider Electric and Telvent: Climbing the Global Smart Grid Ladder . . . and Moving Up Fast!

Initial Impressions – By Chuck Newton

Overall, given the first impression of this prospective corporate marriage, I think that the proposed acquisition of Telvent by Schneider rivals the importance of ABB’s acquisition of Ventyx. In some ways it overshadows that 2010 event. Here’s why:

Schneider is a very large (about $30 billion USD) French-based global corporation headquartered in Rueil-Malmaison, a near-in suburb located just to the west of Paris. The company has recently grown fairly well organically and with a number of strategically well-thought-out acquisitions, including the very visible “AREVA D”, Areva’s medium voltage equipment and systems business, which acquisition was finalized in mid-2010. That acquisition provided the basis for Schneider’s formation of a fifth business sector – “Energy”, reported separately as a line of business for the first time in the company’s 2010 annual report.

However, the Areva D buy-in was just one more drop (albeit a large drop) in the growing bucket of acquisitions recently completed by Schneider Electric. During the past 24 months, the company has acquired the Persian Gulf’s CIMAC (an industrial systems integrator), the SCADAgroup (Australian control systems supplier), Electroshield-TM Samara, (Russia’s largest producer of MV electrical equipment), Conzerve (India-based supplier of industrial energy management schemes) and Microsol Tecnologia (Brazilian supplier of power conditioning equipment); Uniflair SpA, (Italian manufacturer of precision cooling equipment). Schneider further strengthened its hand in building automation and energy efficiency systems with its acquisitions of two French firms, Vizelia (energy management software for commercial buildings) and D5X, specializing in space utilization of commercial buildings.

To continue reading this article in its entirety, jump to Chuck’s Composite page: http://www.newton-evans.com/?page_id=799

Measuring the Impact of GE Energy’s Acquisition of SNC Lavalin ECS Business Unit

August 2, 2010. Well, it was inevitable that GE would make a play for a larger share of the global EMS/SCADA/DMS market and today the company announced the acquisition of the Montreal-based Energy Control Systems business unit of SNC Lavalin. With this acquisition, Newton-Evans believes GE Energy now ranks fourth in the world in terms of numbers of significant energy management, large SCADA and large distribution management systems. Note that the “GENe” name of the ECS’ offerings might just be an added plus!

A few quick facts about the impact of this acquisition:

Continue reading Measuring the Impact of GE Energy’s Acquisition of SNC Lavalin ECS Business Unit

ABB and the Ventyx Acquisition – Why Now, What Next?

By Charles W. Newton, Newton-Evans Research Company, Inc.

(Updated May 7)

The May 2010 announcement of the ABB acquisition of Atlanta-based Ventyx is likely to serve as a wake-up call to the major competitors of ABB in the electric power T&D and operational smart grid market, primarily the likes of Areva T&D, GE and Siemens. This week’s acquisition puts ABB squarely in the heart of “smart grid” activities – both from an operational perspective, where it has been a global market co-leader, and now set to gain a significant market position in the burgeoning enterprise utility “smart grid” software market, a perspective beyond that of any direct competitor.

ABB will now be in a better position for more smart grid-related opportunities than any other of the IT-centric “smart grid” players, none of whom can compete directly in the operational side of “smart grid” with smart field equipment offerings. Overall, this eases the “shopping/procurement” burdens of utilities. The effect of ABB’s acquisition of perhaps the best available and largest independent energy industry applications software provider positions ABB for a larger role in the hundred-billion dollar-plus market for operational equipment and for energy enterprise software.

Continue reading ABB and the Ventyx Acquisition – Why Now, What Next?

Areva T&D Apparently To Remain in French Hands After All

After months of internal debate and consideration of proposals from GE and Toshiba, Areva’s top tier of executives have decided to keep the $7 billion-plus T&D business under French control. AREVA’s Supervisory Board met on November 30, 2009 to examine the bids. After review, the Supervisory Board asked the Executive Board to begin exclusive negotiations with Alstom/Schneider.

The consortium offered 2.29 billion Euros in equity value, i.e. 4.09 billion Euros in enterprise value. The bid does not include any requirement for a seller’s warranty but includes a buyer’s commitment to maintain all European sites for a 3-year period.

To ensure that all AREVA T&D team members are integrated properly, Alstom/Schneider have also agreed to offer to all European employees a similar position in the same geographic area, at an equivalent qualification level and without loss of compensation or seniority.

Finally, unless the economic environment deteriorates significantly, the buyers made a commitment not to implement any layoff program except for voluntary terminations. There are still many unresolved issues including these: Continue reading Areva T&D Apparently To Remain in French Hands After All

summary reviews and highlights from completed studies

summary reviews and highlights from completed studies