Some readers may be unaware that the Agency for International Development (USAID) has planned, developed, managed and executed successful electric power infrastructure development projects in dozens of developing nations over its multi-decade history. USAID had been the world’s premier international development agency, until its near-closure early this year. USAID has been one of three principal approaches to the country’s being held in high regard among other nations, along with Voice of America and the Peace Corps. Begun under President John Kennedy, the Agency for International Development was an outreach that expanded upon Kennedy’s famous statement “Ask not what your country can do for you, but what you can do for your country.” Kennedy’s outlook further expanded to a world view in the context of “…what can America provide to benefit the world.” The nation was energetic and young people stepped up to respond and to propel the country forward on a number of fronts.

The first contact with USAID in my experience was in Vietnam some 58 years ago. I was a young U.S. army specialist/sergeant deployed in villages around and downriver from Saigon. On multiple occasions I would come across USAID truck convoys delivering foodstuffs (including rice, of all things, a somewhat unbelievable commodity to those of us who could see Vietnamese rice paddies just about everywhere in that region of the country) in large sacks that read “From the American People.” A nice sentiment that meant a lot to the nearly three million servicemen and women who served in that conflict and could find something positive in their collective experience via US AID and its courageous efforts to feed many thousands of South Vietnamese citizens.

The U.S. Agency for International Development (USAID) has remained as the principal U.S. agency to extend assistance to countries recovering from disaster, trying to escape poverty, and engaging in democratic reforms. In addition to the provision of foodstuffs and life-saving vaccinations against diseases to millions of people, electrification projects rank among USAID’s many successful undertakings.

USAID supports electrification projects globally, focusing on expanding access to reliable and affordable electricity, particularly in off-grid areas, and promoting sustainable energy solutions, including mini-grids and solar systems.

USAID’s key focus has included these five areas:

Expanding Access to Electricity: USAID aimed to increase access to electricity, especially in underserved areas, by supporting on- and off-grid solutions.

Strengthening Energy Sector Institutions: USAID worked to strengthen the capacity of energy sector institutions to manage and deliver electricity services effectively.

Promoting Private Sector Investment: USAID encouraged private sector involvement in the energy sector to foster sustainable and scalable solutions.

Developing Sustainable Off-Grid Models: USAID supported the development of viable and sustainable off-grid electrification models, including mini-grids and solar systems.

Supporting Clean Energy Technologies: In partnership with the National Renewable Energy Laboratory, USAID has developed ongoing and successful renewable energy programs in at least 13 countries representing nearly one billion people.

Now the real point of this article is simply to make readers aware of the multiple electrification projects that have been successfully undertaken by USAID over the years. Please let your legislators know that it is a mistake to forego these positive developments that cast a bright and positive light on America helping other nations improve access to electricity and thereby putting our country in a good position to win friends and influence governments around the world. If we can’t continue to help our international brothers and sisters, then surely our frenemies will step in and cheer our departure from this charitable component of the American nation on the world scene.

Here is a key example of some remarkable electrification successes attributable to wise research, planning and investment decisions made by USAID management and staff over the past 63 years.

Ukraine: USAID had been helping Ukraine strengthen its power grid, improve energy efficiency, and increase the use of renewable energy sources.

Papua New Guinea: USAID supported the PNG government in its efforts to expand electricity access, with a focus on off-grid solutions and private sector engagement.

South Asia: USAID had been working with countries in South Asia to support their energy sector transformation, including the development of renewable energy and the improvement of energy efficiency.

These efforts have benefited many of the citizens in these and at least a dozen other countries with basic electrification to remote areas, infrastructure electrification of transit and transport systems, upgrading of power lines and substations, and a more positive view of America and Americans. This is one vital approach to keep the U.S. influential and strong among global communities. This is a display of soft power at its finest. Andrew Natsios had served as USAID administrator under President George W. Bush. He recently stated, “USAID is the most pro-business and pro-market of all aid agencies in the world.”

Nonetheless, as I write this article, the administration has apparently concluded its review of USAID, and indicated that just about all of USAID’s programs would be cancelled, involving approximately 5,200 contracts. We who are active participants in the energy industry need to raise our voices in support of USAID and its role in expanding American influence and winning friends for the nation around the world. At the same time, it is important for us to realize that the Voice of America has been another strong component of our foreign policy since the early days of World War II. News of energy developments in the U.S. and worldwide have been among the news stories broadcast over the VOA throughout these last eight decades. While traveling to nearly 135 countries during my own active energy industry research studies over 45 years, I have been made aware of VOA broadcasts listened to by energy industry colleagues in languages ranging from Farsi and Arabic, to Russian, to Chinese and a host of other languages. In some countries, VOA is the only way for citizens to learn about American efforts and progress in sustainable development and obtain a glimpse of world news. VOA has served the world with a consistent message of truth, hope and inspiration. I can vouch for the VOA’s influence on the world community of nations based on my own experiences and travels in countries like Iran, China and Russia as well as much of Asia.

If our Congressional representatives and senators lack the will to raise their voices, then we must rise to do so. Adding the budgets of USAID and VOA together, the total allotment amounts to less than one percent of the federal budget. USAID is looked to by more than a million people around the world involved in sustainable development goals as well as multiple millions who have benefited from an array of successful energy initiatives now fully implemented.

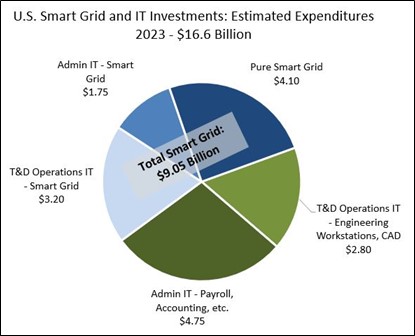

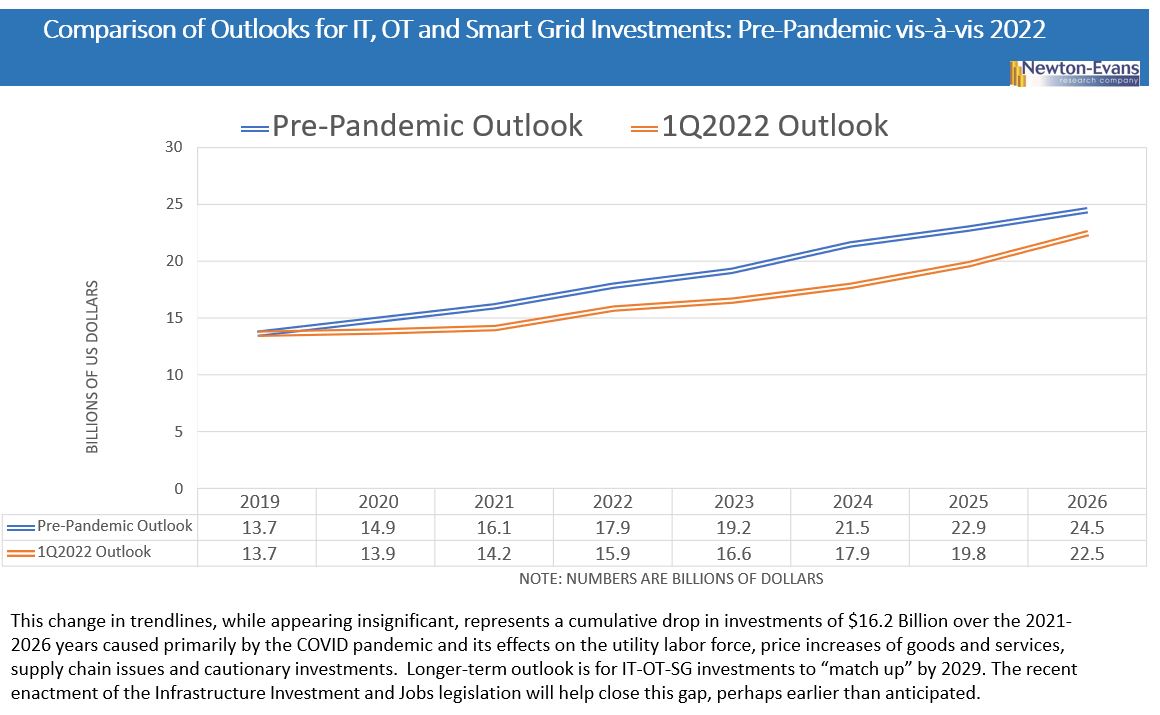

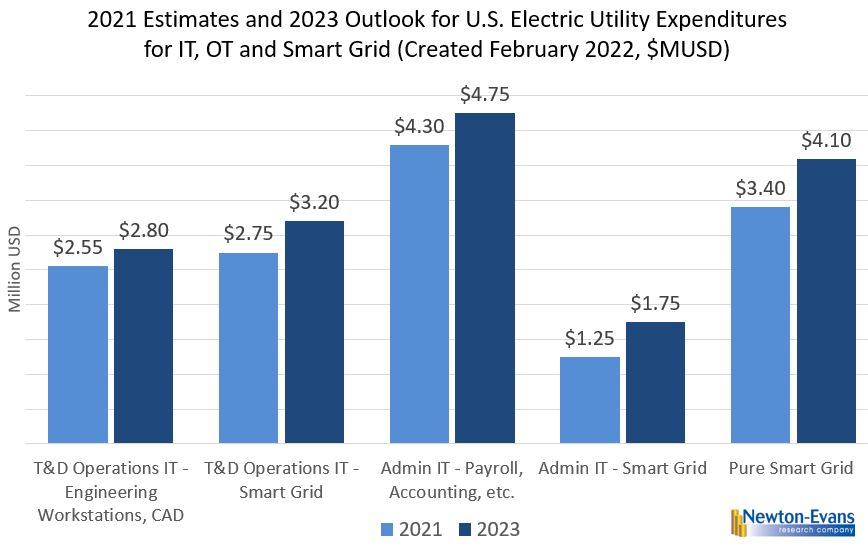

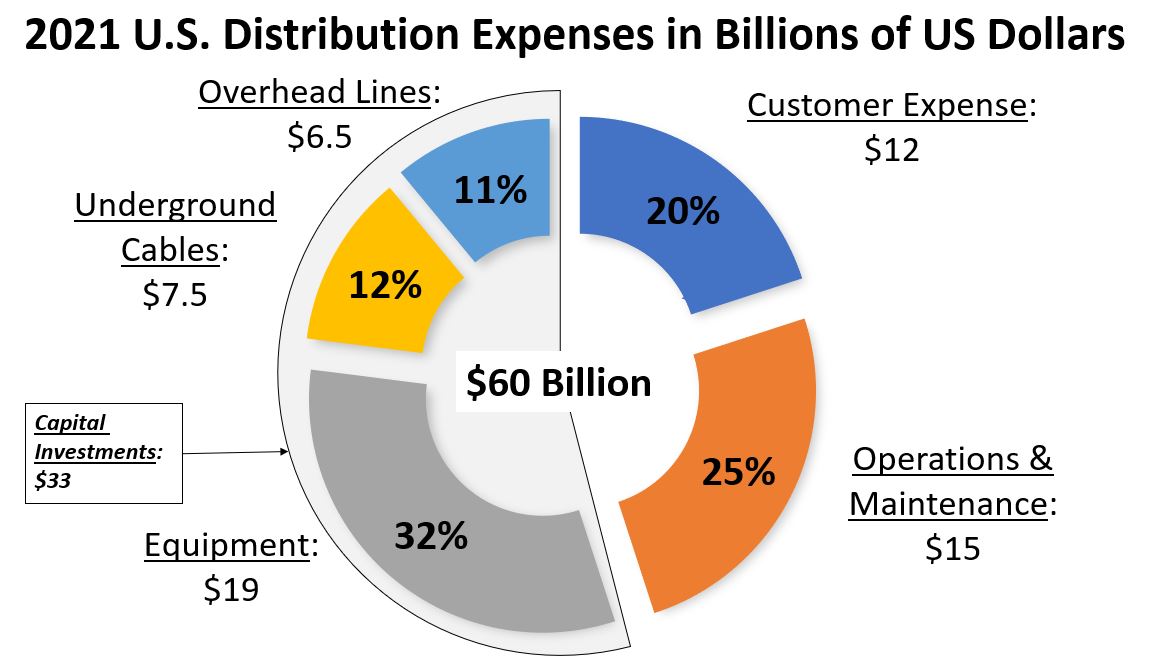

summary reviews and highlights from completed studies

summary reviews and highlights from completed studies